Entrepreneurial finance

Lecture 5: Managing Finances Part 2

The purpose of the learning is for you to develop your own learning. There are a number of tasks that you should complete before you undertake the next section. You can work through this section at your own pace. It is expected that you would take up to 3 hours to complete this section. You must complete this section before you move to the next section.

Task 1

You need to open and listen to “Lecture 5” presentation

This presentation introduces the three most important financial reports for a start-up or small business

Task 2

You should now complete the questions in your workbook

These questions will build your knowledge of entrepreneurial finance.

Task 3

You should open the document “Understanding Spreadsheets”

This document provides an explanation on how to complete cash flow, profit and loss and balance financial reports

Understanding Spreadsheets

We mentioned in the previous presentation that there are three critical financial reports that every business owner needs to understand as they provide critical information about the status of the business and how they can survive. These reports are Cash Flow, Profit and Loss and Balance report.

Cash flow

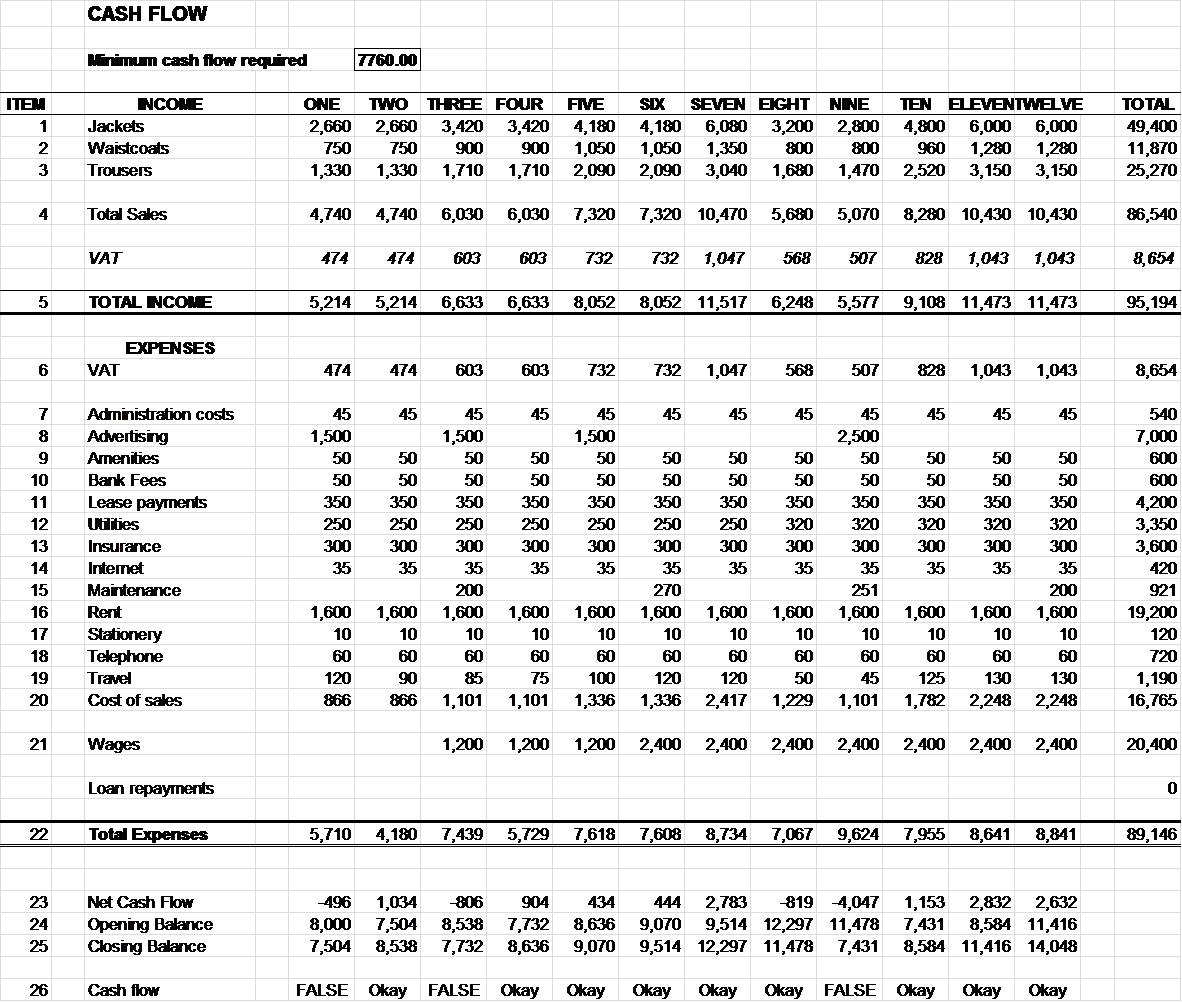

You cash flow report shows you how your money is moving in and out of your business. It also gives you a running total of how much you have in the bank. You should use your cash flow report to reconcile you bank statements and to track your payments and income. Below is a typical cash flow report for a new small business that makes men’s suits at the end of their first year trading.

Across the top of the spreadsheet you will see the numbers one to twelve, this represents each month of trading. The minimum cash flow at the top left side is the minimum working capital needed to stay open. On the left hand side you will see Item numbers. The table below explains what each number means and how it was calculated.

| ITEM | DETAILS |

| 1 | This is the total income or sales for Jackets for each of the twelve months.

|

| 2 | This is the total income or sales for Waistcoats for each of the twelve months.

|

| 3 | This is the total income or sales for Trousers for each of the twelve months.

|

| 4 | This is the sum of all the sales for each month for the Jackets, Waistcoats and Trousers. It does not include any sales or value added tax.

|

| 5 | This is the total income for all sales including sales or value added tax. This is the total amount of money that came into the business.

|

| 6 | This is the amount of sales tax or value added tax that the business has to pay the government. It is calculated in this cash flow at 10%.

|

| 7 | This is the monthly cost for administration; it might include things like the cost of accounting software. In this business it also included things like pins and tailors chalk.

|

| 8 | This is the cost of advertising the business. You should note that it is not a consistent amount for each month.

|

| 9 | This covers the cost of things like toilet paper, cleaning products and tea or coffee.

|

| 10 | This is the charges levied by the bank for holding a business account.

|

| 11 | The owner of the business opted to lease the sewing machines, irons and clothing press, as well as a computer and this is the monthly cost of that lease.

|

| 12 | Utilities covers costs such as water, electricity and waste collection

|

| 13 | The insurance costs cover against loss of the material or equipment, through theft or fire. It also covers loss of income if the business owner was to fall sick and was unable to work.

|

| 14 | This covers access to the internet and emails

|

| 15 | The business owner spent this amount as a fixed maintenance cost to cover any repairs necessary to the equipment.

|

| 16 | The business owner rents a space to make and sell their suits.

|

| 17 | There is a small cost for stationery which includes paper, ink envelopes.

|

| 18 | The telephone costs are on a fixed contract and this represents the amount paid each month.

|

| 19 | Travel is a fixed rate to use an external contract to deliver the suits to the customer.

|

| 20 | The costs of sales are the total amount of material used in making the suits. This is calculated when you are drawing up your marketing or operations plan. |

| 21 | This is the monthly wages paid. In the first two months there are no wages paid. This is because the owner was able to not pay them self a wage. In month Six sales increased so the business owner had to employ an assistant.

|

| 22 | This is the total expenses for each month. This is the total amount of money that went out of the business.

|

| 23 | This is the income minus the expenses. You can see it is a negative number in the seven of the twelve months. However, as the owner invested £15,000 in the business at the start they are able to pay their bills even if more money goes out than comes in.

|

| 24 | This is the amount of money that the business owner invested into his business at the start and is the opening balance in their bank account.

|

| 25 | This is the opening balance minus the net cash flow

|

| 26 | This tells the business owner if the amount of money they have in the bank is equal to or greater than the minimum net working capital to stay open. If it says false it means that the cash reserve has fallen below the minimum net working capital.

|

Analysing the Cash Flow

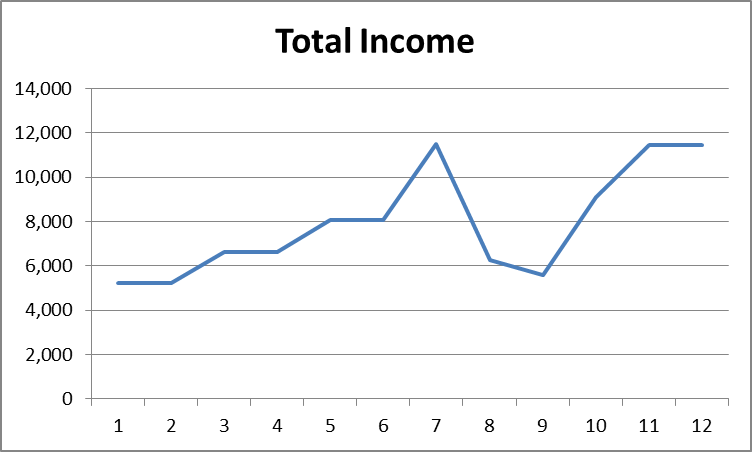

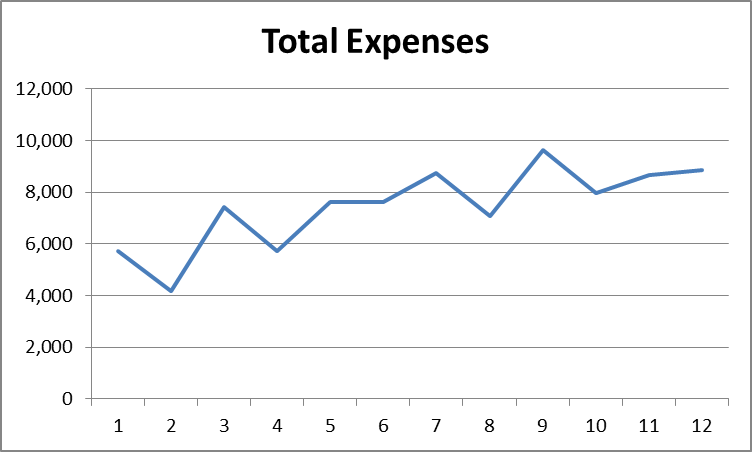

There are a number of points we can draw from this cash flow. Below is two graphs, one of income and one of expenses.

It is clear from the graphs that the income pattern and the sales do not match. What this tells us is the owner needs to ensure that he has coverage during the months that sales drop. The owner can use this information to adjust the levels of inventory, or change the timing of their advertising programme.

The table below was taken from the bottom of the spread sheet and also provides some critical information.

The data in the table above suggests that the initial investment might not have been enough as during months one, three and nine the business much less money coming in than going out. The owner would need to consider some actions to ensure that this improves either by investing more of their own money, taking out a loan, securing an overdraft with the bank, increasing profitability or reducing costs.

Profit and Loss

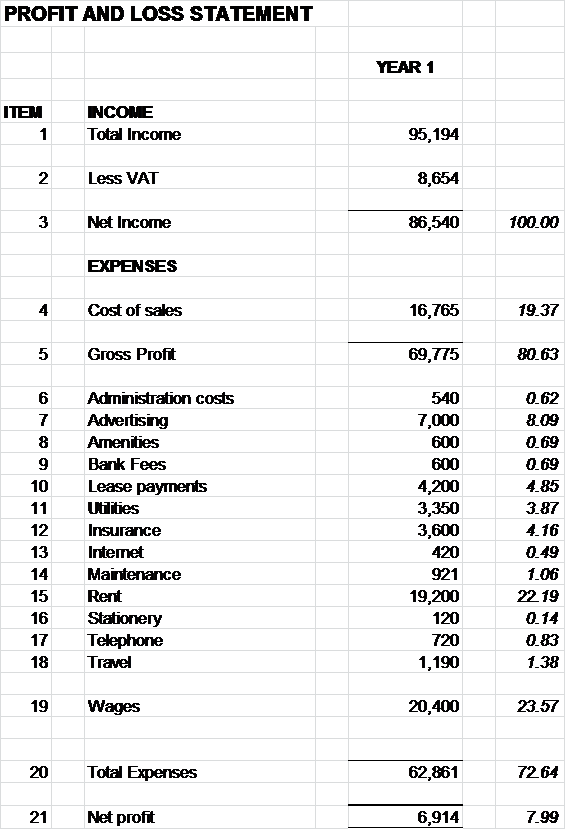

Below is the profit and loss report for the business at the end of the first year trading. It shows you if the business has made a profit or a loss, and it shows you the percentage of each transaction against the income.

The two columns of figures on the right side are related to the income and expenses. The second to last column is the actual cash amounts and the last column is what those amounts are in terms of a percentage of the total income. On the left hand side you will see Item numbers. The table below explains what each number means and how it was calculated.

| ITEM | DETAILS |

| 1 | This is the total income for all sales including sales or value added tax. This is the total amount of money that came into the business.

|

| 2 | This is the amount of sales tax or value added tax that the business has to pay the government. It is calculated in this Profit and Loss at 10%.

|

| 3 | This is the sum of all the sales for each month for the Jackets, Waistcoats and Trousers. It does not include any sales or value added tax. It is presented as 100% of the income. It is often referred to as the net income.

|

| 4 | The costs of sales are the total amount of material used in making the suits. In this Profit and Loss it represents 19.37% of the income.

|

| 5 | This is the total amount after VAT or sales tax and the cost of the material has been deducted. Generally it is referred to as Gross Profit. In this Profit and Loss it represents 80.63% of the income.

|

| 6 | This is the total cost for administration. It is calculated at 0.62% of the Gross profit.

|

| 7 | This is the total cost of advertising the business. It is calculated at 8.09% of the Gross profit.

|

| 8 | This covers the cost of things like toilet paper, cleaning products and tea or coffee. It is calculated at 0.69% of the Gross profit.

|

| 9 | This is the charges levied by the bank for holding a business account. It is calculated at 0.69% of the Gross profit.

|

| 10 | The owner of the business opted to lease the sewing machines, irons and clothing press, as well as a computer and this is the monthly cost of that lease. It is calculated at 4.85% of the Gross profit.

|

| 11 | Utilities cover costs such as water, electricity and waste collection. It is calculated at 3.87% of the Gross profit.

|

| 12 | The insurance costs cover against loss of the material or equipment, through theft or fire. It also covers loss of income if the business owner was to fall sick and was unable to work. It is calculated at 4.16% of the Gross profit.

|

| 13 | This covers access to the internet and emails. It is calculated at 0.49% of the Gross profit.

|

| 14 | The business owner spent this amount maintaining any repairs necessary to the equipment. It is calculated at 1.06% of the Gross profit.

|

| 15 | The business owner rents a space to make and sell their suits. It is calculated at 22.19% of the Gross profit.

|

| 16 | There is a small cost for stationery which includes paper, ink and envelopes. It is calculated at 0.14% of the Gross profit.

|

| 17 | The telephone costs are on a fixed contract and this represents the amount paid each month. It is calculated at 0.83% of the Gross profit.

|

| 18 | Travel is a fixed rate to use an external contract to deliver the suits to the customer. It is calculated at 1.38% of the Gross profit.

|

| 19 | This is the monthly wages paid. In the first two months there are no wages paid. This is because the owner was able to not pay them self a wage. In month Six sales increased so the business owner had to employ an assistant. It is calculated at 23.57% of the Gross profit.

|

| 20 | This is the total expenses for each month. This is the total amount of money that went out of the business. It is calculated at 72.64% of the Gross profit.

|

| 21 | This is the profit the business has made during the first year of trading. It is calculated at 7.99% of the Gross profit. |

Analysing the Profit and Loss

From the percentages we can see that the three biggest expenses are wages, rent and the material to make the suits. However, they may in fact be quite low compared to similar businesses. We mentioned earlier in another lecture that benchmarking is an important activity. In this particular case the owner could compare average wage costs against similar businesses and discover that their wage costs are lower than average, while comparing rent and material costs they may be higher than average. The business owner needs to think about the implications of this. Paying lower than average salaries or wages may mean lower skilled workers while paying higher costs for material may mean they are being over charged. Just like the cash flow this profit and loss report allows the owner to make some critical decisions about the way they are running the business.

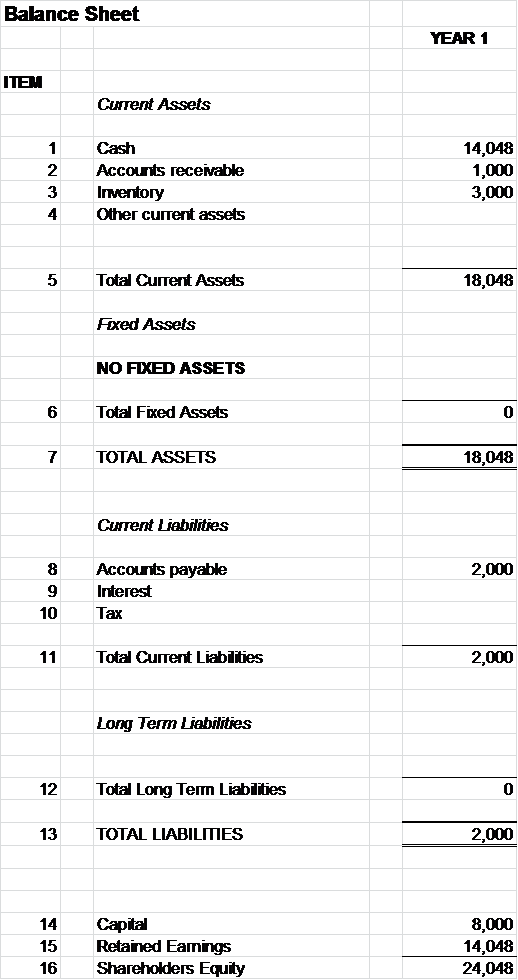

Balance Report

The Balance report shows the value of the business and is constructed from the cash flow report and the profit and loss report. Below is the balance report for the tailor at the end of their first year trading.

Task 4

You should now complete the questions in your workbook

These questions will build your knowledge of entrepreneurial finance.

Task 5

You should watch the following two videos Cash Flow 1 and Cash Flow 2

These videos will give you a deeper understanding of cash flows

Task 6

You should watch the following two videos Profit and Loss 1 and Profit and Loss 2

These videos will give you a deeper understanding of Profit and Loss

Task 7

You should watch the following video Balance Report

These videos will give you a deeper understanding of Balance Report

You should undertake further reading on the topics in this section. We recommend that you read the following:

Chapter 3: Adelman, P. and Marks, A. (2014) Entrepreneurial Finance, 6th edition, Pearson Education, New Jersey.

You will find the following links useful:

Accounting and Finance dictionary

You should watch the following videos

The next section is Lecture 6

Introduction to the module

Welcome to module “Entrepreneurial finance”.

Download here related workbooks before starting the course:

All workbooks in this course please submit to I.Ekanem@mdx.ac.uk (MDX students), apenafiel@uma.es (UMA students), marko.cular@efst.hr (UNIST students), upon finishing the assignments.

About author

Dr. Ignatius Ekanem is a Senior Lecturer in Business Management and Director of Programmes at Middlesex University, London. He has a wealth of experience of teaching at undergraduate and postgraduate levels and PhD supervision. He is a programme leader for BA Business Management (Innovation) and a module leader for Enterprise and Small Business and for Small Business Going Global.

Previously, he worked as a Senior Researcher at the University’s Centre for Enterprise and Economic Development Research (CEEDR), specialising in economic regeneration, with a particular focus on the financial management practices of small businesses. During his time with CEEDR, Ignatius worked on a series of research projects including several studies for the Small Business Service on social enterprise, ethnic minority owned businesses and rural enterprises. He also worked on the demand and supply of finance and business support for ethnic minority businesses commissioned by the British Bankers Association, the Bank of England and the Small Business Service.

His most recent projects include ‘The impact of perceived access to finance difficulties’ commissioned by the Small Business Service; ‘Access to Bank Finance for Scottish SMEs’ (for The Scottish Government); and an assessment of the government’s equity finance initiatives for SMEs with growth potential (for the Department for Business, Innovation and Skills).

He has published in reputable journals, including The British Accounting Review, International Small Business Journal, Journal of Small Business and Enterprise Development and International Journal of Consumer Studies. He has written two book chapters, three inspirational books and is a co-author of over 20 official reports. Ignatius has also written and presented many conference papers both in the UK and internationally, including the USA, Canada, Australia and South Korea

For discussion and course related questions visit the FORUM.

Course Features

- Lectures 6

- Quizzes 0

- Duration 60 hours

- Skill level All levels

- Language English

- Students 13

- Assessments Self

-

UNIT 1

- Lecture 1.1 Lecture 1: Sources of Entrepreneurial Finance

-

UNIT 2

- Lecture 2.1 Lecture 2: Financing Gap

-

UNIT 3

- Lecture 3.1 Lecture 3: Working Capital Management

-

UNIT 4

- Lecture 4.1 Lecture 4: Managing Finances Part 1

-

UNIT 5

- Lecture 5.1 Lecture 5: Managing Finances Part 2

-

UNIT 6

- Lecture 6.1 Lecture 6: Managing Finances – Ratios