Entrepreneurial finance

Lecture 2: Financing Gap

The purpose of the learning is for you to develop your own learning. There are a number of tasks that you should complete before you undertake the next section. You can work through this section at your own pace. It is expected that you would take up to 3 hours to complete this section. You must complete this section before you move to the next section.

Task 1

Read the lecture “Finance gap ”

This lecture introduces the concept of a finance gap. This is the gap between the amount of money you need to start a business and the amount of money you have access to.

LECTURE 2: FINANCE GAP

A finance gap arises if the demand from small firms for finance is greater than the willingness of financial institutions to supply it at current market conditions.

Finance gaps are often interpreted as being the result of the ‘information asymmetry problem’ (i.e. entrepreneurs know more about themselves and their businesses than it is possible for the lending organisations to have of them) – this problem reflects difficulties in communication and credibility.

Information asymmetry leads to two problems for a bank:

- Adverse Selection: Finance for a business that subsequently fails or no finance for a business that would have been successful.

- Moral Hazard: a monitoring problem – owner-manager not acting in the best interest of the bank once loan is raised. Hence the requirement for security.

According to some sources, one of the most consistent themes in discussions about small business finance in the UK is whether or not there are ‘gaps‘ in the market which justify intervention. He distinguishes:

- Supply side failure: where proposals are turned down for reasons not connected with the viability of the proposal itself (such as firm’s lack of a track record)

- Demand side failure: where firms do not properly exploit the financial opportunities available because of a lack of knowledge, poor management or inadequately presented proposals

- Complete market failure: where firms are not offered any finance for reasons that are not connected with the viability of either the proposal or the business

Finance gaps have been recognised in the UK for over 70 years, being first identified by the Macmillan Report of 1931 – this found that small firms had difficulty in raising amounts of less than £200,000 (equivalent to £4 million today).

The Wilson Committee (1979) concluded that small firms were at a disadvantage compared with large firms in terms of the cost of loan finance and the security required to obtain it. Because of the particular problems faced by new firms, Wilson recommended a Small Firms Loan Guarantee Scheme

Recent empirical evidence on the finance issue varies according to the precise questions asked and the composition of the sample. For example, University of Cambridge Business Research Survey of 2064 firms in the UK found that 23% of them considered the cost of finance for expansion to be a constraint on meeting business objectives; this being the 4th most commonly identified constraint.

The behaviour and practices of both lenders and small businesses may contribute to both supply and demand side failure:

- Banks emphasis on a collateral approach to lending may contribute to supply side failure if otherwise viable business propositions are being turned down. The banks justify such an approach in terms of the high cost of acquiring the information required to make a business risk assessment.

- A key issue from banks perspective results from the way in which propositions are presented and the poor quality of financial data presented to support loan applications (demand side failure)

Such imperfections in the market are most evident in the case of certain types of small businesses:

- new firms: because of their lack of a track record and frequent lack of collateral which can make them a high risk lending proposition (although a scheme like the LGS was introduced to attempt to address this) (North et al., 2010)

- young rapidly growing firms: their demands for external finance may exceed the willingness of financial institutions to supply it, possibly because they have already borrowed up to the limit of their security

- –some ethnic minority firms: because of the way in which cultural factors can affect the relationship between the small firm and lending institutions (North et al., 2010).

- young high technology businesses: because of a combination of the scale of their financial needs and the risk, which is associated with the delay in generating a financial return

- small businesses in deprived areas: lack of business experience; lack of collateral & personal equity; concentration in sectors with high failure rates; small and localised markets; areas with high crime rates; lack of training and advice.

- female entrepreneurs: lack of advice about options/finance sources; feeling they would be turned down; poor credit history

Below are some tables that demonstrate the issues around the finance gap.

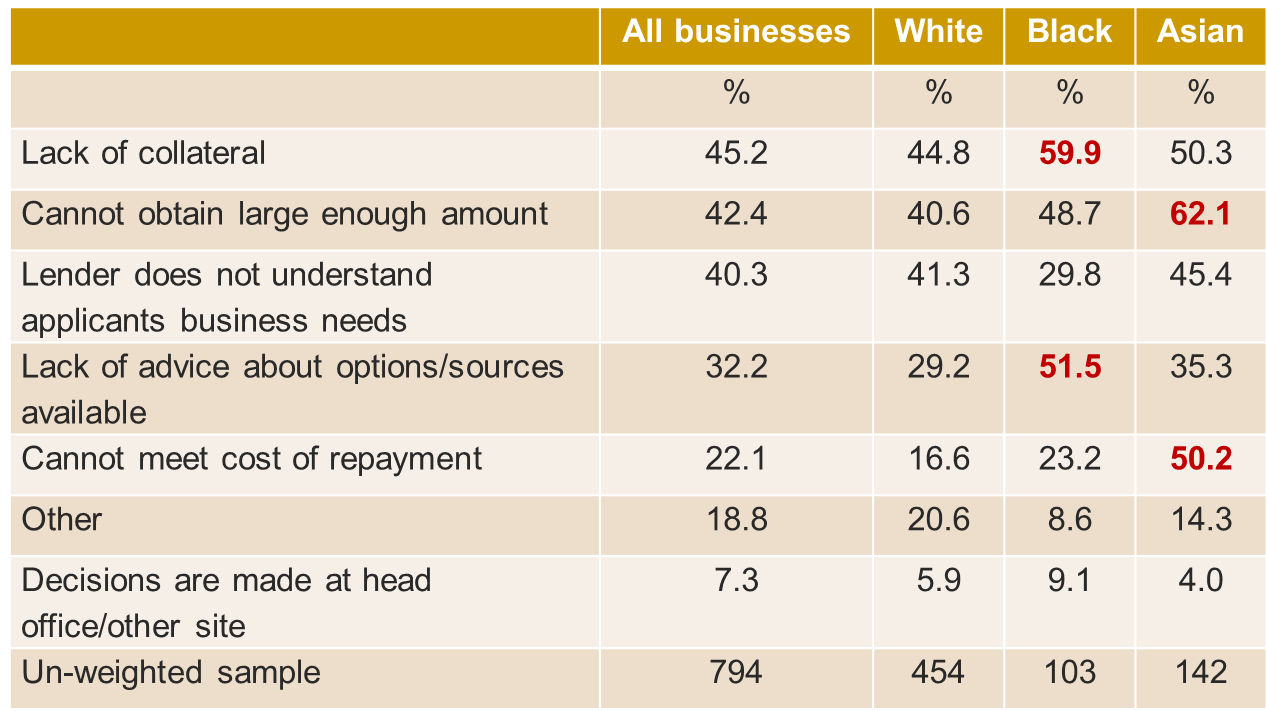

Problem in accessing external finance by ethnicity for London SMEs

The table above shows the difficulties that different businesses have when trying to access finance. The sample is also broken down by ethnicity. The most common issue that prevents business from getting finance is a lack of collateral. Generally the least common is that the borrower is perceived as not being able to meet the repayments. However, this is a much lower issue for borrowers from a white ethnic background. These figures clearly show that ethnicity plays an unfortunate role in financing small businesses.

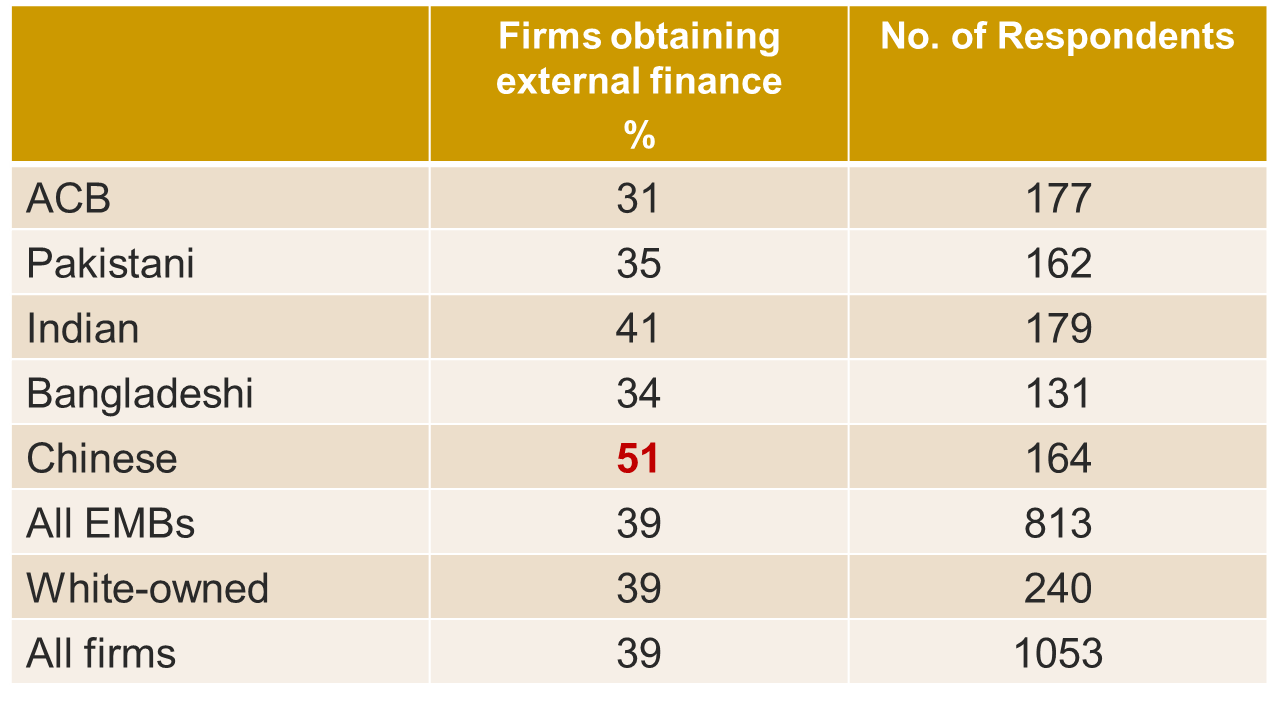

External finance from formal sources at start-up

(i.e. finance other than from own savings, family and friends)

This table shows the number of start-ups that are funded using external sources. As you can see the overall number and the number for each ethnicity except Chinese is below 50%. Clearly finance from external sources is not the way the majority of business start-ups are funded.

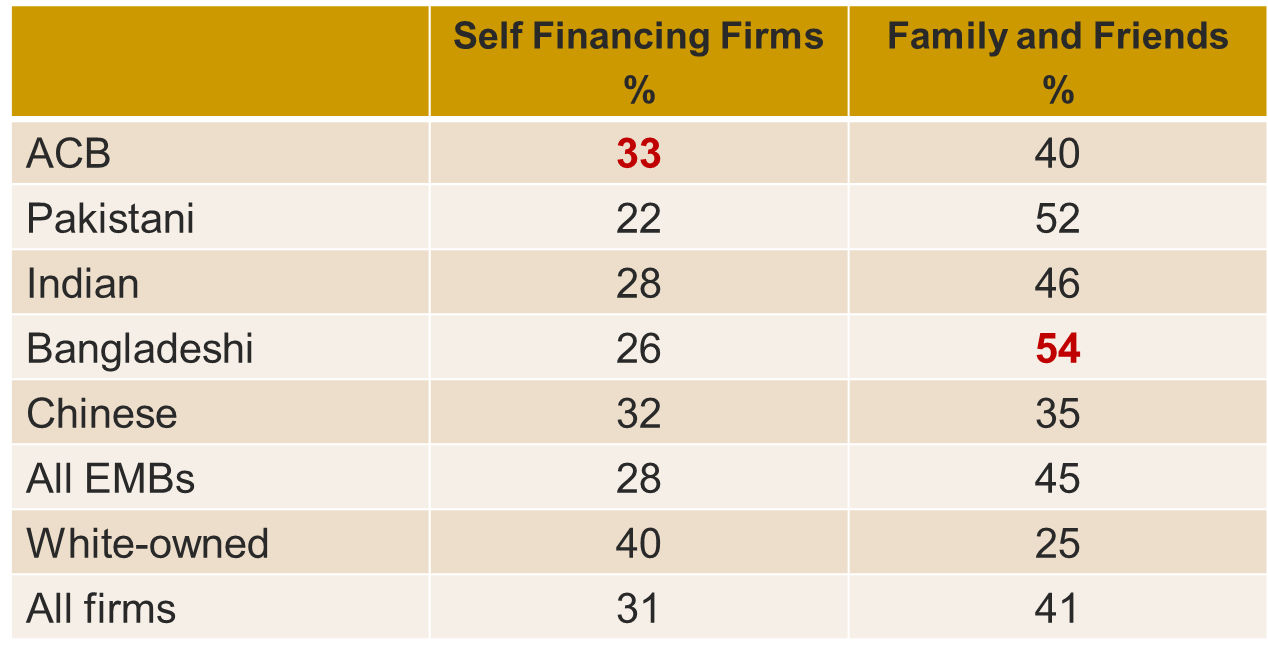

Proportion of firms using self-financing and / or family and friends at start-up

This table shows the distrubtion across ethnicities the about of funding that comes from either the owner or family and friends. When you contrast this table with the second table is it is clear that the vast majortiy of start-ups use either their own money or borrow from family and friends.

Task 2

You now need to watch this online video

This video looks the finance gap in more detail.

Task 3

If you have access you should now read Chapter 7: Deakins, D and Freel, M. (2012) Entrepreneurship and Small Firms, 6th edition, McGraw-Hill, London.

This provides a broader explanation of the issues caused by a finance gap

Task 4

You should now answer the questions in your workbook.

This enables you to develop your learning further.

You should undertake further reading on the topics in this section. We recommend that you read the following:

Chapter 7: Deakins, D and Freel, M. (2012) Entrepreneurship and Small Firms, 6th edition, McGraw-Hill, London.

You will find the following links useful:

Accounting and Finance dictionary

The next section Lecture 3

Introduction to the module

Welcome to module “Entrepreneurial finance”.

Download here related workbooks before starting the course:

All workbooks in this course please submit to I.Ekanem@mdx.ac.uk (MDX students), apenafiel@uma.es (UMA students), marko.cular@efst.hr (UNIST students), upon finishing the assignments.

About author

Dr. Ignatius Ekanem is a Senior Lecturer in Business Management and Director of Programmes at Middlesex University, London. He has a wealth of experience of teaching at undergraduate and postgraduate levels and PhD supervision. He is a programme leader for BA Business Management (Innovation) and a module leader for Enterprise and Small Business and for Small Business Going Global.

Previously, he worked as a Senior Researcher at the University’s Centre for Enterprise and Economic Development Research (CEEDR), specialising in economic regeneration, with a particular focus on the financial management practices of small businesses. During his time with CEEDR, Ignatius worked on a series of research projects including several studies for the Small Business Service on social enterprise, ethnic minority owned businesses and rural enterprises. He also worked on the demand and supply of finance and business support for ethnic minority businesses commissioned by the British Bankers Association, the Bank of England and the Small Business Service.

His most recent projects include ‘The impact of perceived access to finance difficulties’ commissioned by the Small Business Service; ‘Access to Bank Finance for Scottish SMEs’ (for The Scottish Government); and an assessment of the government’s equity finance initiatives for SMEs with growth potential (for the Department for Business, Innovation and Skills).

He has published in reputable journals, including The British Accounting Review, International Small Business Journal, Journal of Small Business and Enterprise Development and International Journal of Consumer Studies. He has written two book chapters, three inspirational books and is a co-author of over 20 official reports. Ignatius has also written and presented many conference papers both in the UK and internationally, including the USA, Canada, Australia and South Korea

For discussion and course related questions visit the FORUM.

Course Features

- Lectures 6

- Quizzes 0

- Duration 60 hours

- Skill level All levels

- Language English

- Students 13

- Assessments Self

-

UNIT 1

- Lecture 1.1 Lecture 1: Sources of Entrepreneurial Finance

-

UNIT 2

- Lecture 2.1 Lecture 2: Financing Gap

-

UNIT 3

- Lecture 3.1 Lecture 3: Working Capital Management

-

UNIT 4

- Lecture 4.1 Lecture 4: Managing Finances Part 1

-

UNIT 5

- Lecture 5.1 Lecture 5: Managing Finances Part 2

-

UNIT 6

- Lecture 6.1 Lecture 6: Managing Finances – Ratios